Aniline Market Insights by Application and End-Use Industry

Report Overview:

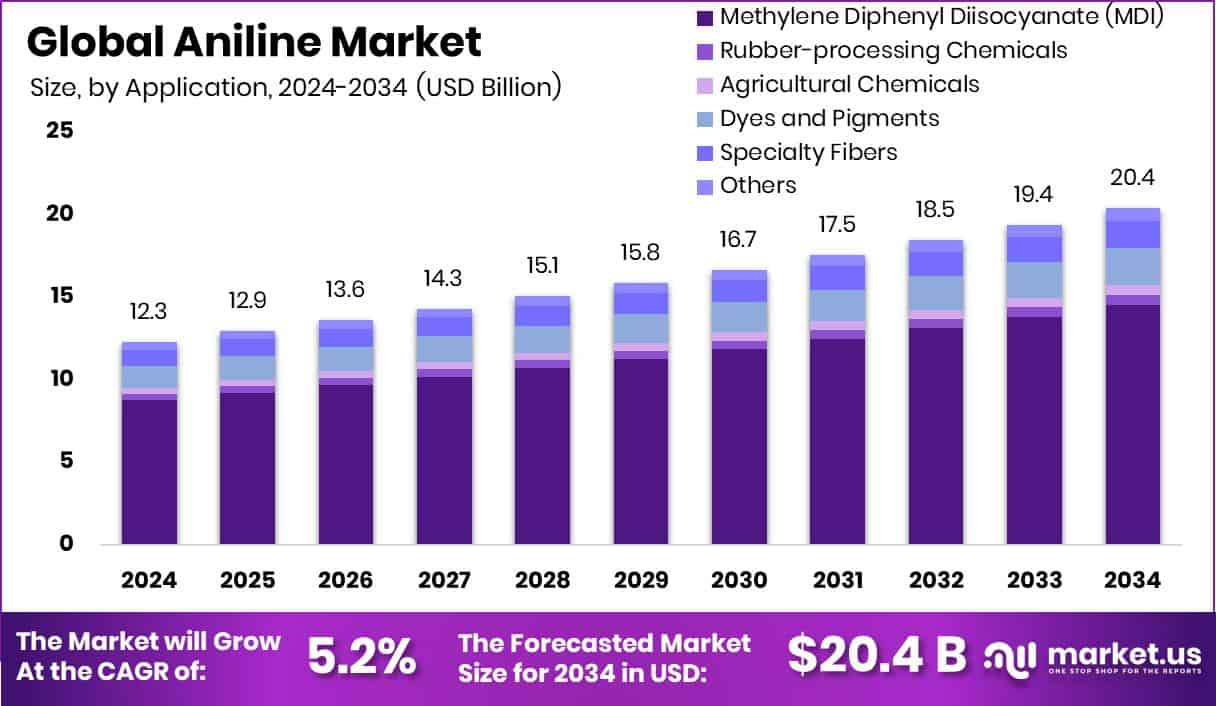

The global aniline market was valued at approximately USD 12.3 billion in 2024 and is anticipated to grow to roughly USD 20.4 billion by 2034, exhibiting a CAGR of 5.2% over the 2025–2034 period. Aniline (C₆H₅NH₂), typically a clear or slightly yellow liquid with a characteristic odor, is produced via reduction of nitrobenzene and acts as the essential building block across multiple industries. Its primary applications include MDI production for polyurethane foams, rubber‑processing chemicals, dyes, herbicides, and pharmaceutical intermediates. The growing demand is fueled by expansion in construction and automotive sectors especially in Asia‑Pacific where polyurethane based insulation, seating and furniture components are widely used. Asia‑Pacific accounted for around 44.2% of global market share in 2024, supported by urbanization and infrastructure growth in countries like China and India.

By application, MDI (methylene diphenyl diisocyanate) dominates, accounting for ~71.2 % of total usage, mainly in insulation, automotive seating, and furniture foams. Other applications such as synthetic dyes, rubber‑processing additives, agrochemical intermediates, and pharmaceutical precursors make up the remaining share. In distribution channels, direct industrial sales lead with approximately 71.8 % share, reflecting bulk procurement by manufacturers. Regionally, Asia‑Pacific held the largest share (~44.2%) in 2024, driven by robust demand in construction, automotive, textile, and agro‑industries; North America and Europe follow with mature but growing demand bases. Factors driving growth include rising demand for polyurethane in construction and automotive sectors, while restraints include supply chain volatility and regulatory challenges. Opportunities lie in emerging markets and value‑added derivative applications, supported by evolving trends toward more eco‑friendly and bio‑based production processes.

Key Takeaways

Market value rose from USD 12.3 billion in 2024 to projected USD 20.4 billion by 2034.

MDI applications dominate consumption (~71.2% of aniline usage).

Direct sales account for the majority distribution (~71.8% share).

Asia‑Pacific leads regionally with about 44.2% of the market share.

Growth underpinned by expanding construction and automotive sectors.

Download Exclusive Sample Of This Premium Report: https://market.us/report/global-aniline-market/free-sample/

Key Market Segments:

By Application

- Methylene Diphenyl Diisocyanate (MDI)

- Rubber-processing Chemicals

- Agricultural Chemicals

- Dyes and Pigments

- Specialty Fibers

- Others

By End-use

- Building and Construction

- Rubber

- Consumer Goods

- Automotive

- Packaging

- Agriculture

- Others

By Distribution Channel

- Direct Sales

- Distributors/Wholesalers

- Online Retailers

- Specialty Stores

- Chemical Supply Chains

- Others

DORT Analysis

Drivers

The primary driver is surging demand for MDI based polyurethane foams, especially in insulation, automotive seating, and furniture manufacturing. Rapid urbanization, infrastructure investment, and growth in building activity in Asia drive large scale demand. The textile and agrochemical segments also steadily consume aniline via dyes and herbicide intermediates. Growing industrial consumption in developing markets further sustains upward momentum.

Opportunities

Emerging markets such as India and Southeast Asia offer large untapped potential as construction and automotive sectors expand. Increasing interest in bio‑based and greener production processes opens innovation pathways. Development of specialty derivatives beyond MDI, such as pharmaceuticals or advanced dyes, offers value‑added growth. Investment in local production capacity in underserved regions can reduce import dependency and improve margins.

Restraints

Stringent environmental and safety regulations around aniline production raise compliance costs for producers. Volatility in benzene feedstock and crude oil prices can squeeze profit margins. Intense competition and overcapacity in some regions may limit pricing power. Health concerns (e.g. methemoglobinemia risk) may restrict usage or prompt tighter controls, slowing market uptake.

Trends

Growing adoption of sustainable production methods, like bio‑based aniline, is emerging. Automation and advanced catalysis are improving process efficiency and lowering waste. Increasing vertical integration among chemical producers to control MDI supply chains. Shift toward stricter environmental compliance and cleaner chemistry is transforming product offerings.

Market Key Players:

- BASF Corporation

- BONDALTI

- Borsodchem Mchz

- Covestro AG

- Dow

- GNFC

- Huntsman International LLC

- Jilin Connell Chemical Industry Co., Ltd.

- Mitsubishi Chemical

- Mitsui Chemical

- Petrochina Co. Ltd.

- Sabic

- SP Chemicals Holdings Ltd.

- Sumika Bayer Urethane Co., Ltd.

- Sumitomo Chemical Co. Ltd.

- The Dow Chemical Company

- Wanhua Chemical Group Co. Ltd.

Comments

Post a Comment